The athleisure segment has had mixed fortunes. While highfliers such as Lululemon (NASDAQ:LULU) continue to post amazing growth, other players have stumbled. Today, there are several undervalued athleisure stocks to consider.

Broadly, the athleisure segment has been a growing category for several reasons. First, the work-from-home trend catalyzed by the Covid-19 pandemic has been a boost. It has reduced the demand for official wear. After all, with business meetings happening via video calls in our homes, loungewear, leggings and sweatpants do the job!

Secondly, the fitness and active lifestyle trend has promoted growth. Indeed, this trend will continue to drive growth for athleisure stocks. The global athleisure market will grow at a 9% compounded annual growth rate, reaching a $662 billion market size by 2030.

These growth tailwinds will buoy the entire industry including these undervalued athleisure stocks to buy. Although some athleisure brands have had execution issues, the work-from-home and fitness trends will be a growth driver. Buy these three undervalued athleisure stocks to profit.

Nike (NKE)

This athleisure giant is one of the first names to consider. No doubt Nike (NYSE:NKE) has stumbled in recent quarters due to an inventory glut. However, these issues are temporary and the long-term opportunity remains compelling.

Indeed, in recent quarters, Nike’s struggles have been self-inflicted. Due to soaring demand during the pandemic lockdowns, there was excessive ordering from factories. However, as economies reopened and spending shifted to services from goods, supply became elevated. Excess inventory became a headwind in 2023, forcing the company to heavily discount prices.

As a result, financial results in 2023 were underwhelming. The latest Q2 FY2024 results disappointed, with North American sales declining 4% year-over-year. Another source of weakness has been in what was once its greatest strength—China. Economic problems in the country have lowered consumer confidence, reducing overall spending. Sales in the country only grew 4% YOY in the quarter.

Putting Nike’s fundamental performance into perspective, the abovementioned headwinds are temporary. First, the company has already made progress in reducing inventory to an optimal level. The company ended Q2 FY2024 with $8 billion in inventory, down 14% YOY. Therefore, gross margins could inflect higher in coming quarters.

Secondly, the Chinese market still represents a substantial opportunity as more people join the middle class. The Communist Party has already taken measures to boost the economy and confidence. Thirdly, the company has announced a $2 billion cost-saving plan to improve profitability.

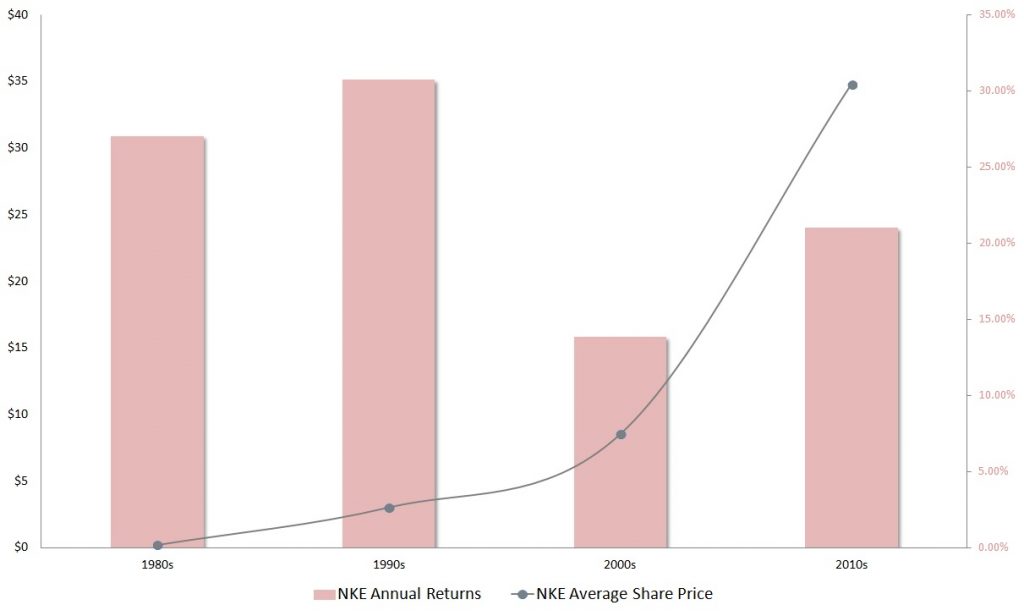

As of this writing, Nike is one of the most undervalued athleisure stocks. Despite its premium brand positioning and historical earnings quality, it trades for 23 times forward earnings. The time to buy NKE is now before conditions improve. The stock will be off to the races soon after China and North America inflect.

Lululemon (LULU)

Lululemon (NASDAQ:LULU) is another stock to consider as the innovative leader in the category. The athleisure giant has been a trendsetter in the category. Still, it continues to lead with innovative designs and expand into new areas.

Intuitively, it is easy to regard the athleisure stock as expensive based on metrics like price-to-earnings. However, remember that it has been one of the fastest-growing brands. The company achieved 25% annual sales growth over the past five years. Therefore, paying up a bit for the premium growth is worthwhile.

In terms of valuation, LULU stock trades for 32 times forward earnings. That’s a cheap multiple for a stock that has grown EPS by 28% annually over the last five years. According to Finviz, the stock will increase EPS by 17% annually over the next five years.

The company’s Power of Three ×2 growth plan, unveiled in April 2022, underpins its ambition. It plans to double men’s revenue by 2026 and continue the momentum in digital sales. The company also plans to double international revenues through expansion in China, Asia Pacific and Europe.

The company has already updated earnings expectations for Q4 FY2023, projecting 14% to 15% revenue growth. That’s one of the highest growth rates among undervalued athleisure stocks. The growth story will continue to push this stock higher.

Under Armour (UAA, UA)

This athleisure brand is a turnaround story with substantial upside. Under Armour (NYSE:UAA, NYSE:UA) is one of the most undervalued athleisure stocks based on valuation metrics alone. Management’s FY2024 outlook forecasts $0.57 to $0.59 in diluted EPS, meaning the stock trades for 14 times forward earnings.

The company has done a great job of rightsizing its inventory. In Q3 FY 2024, inventories were down by 9% YOY to $1.1 billion. However, revenue growth is a work in progress, especially in North America. Management is working on reviving the brand in the region, led by new CEO Stephanie Linnartz, who took over in February 2023. The company has already revamped two-thirds of its executive team, bringing in fresh blood.

Under Armour is still a premium brand relevant to the athleisure market. A great example is the Curry brand, which the popular Curry 11 Basketball Shoe headlines. Building on the strength of this brand with exciting collaborations is an opportunity.

The company also plans to refresh its product line by the spring and summer this year. It expects key products like the Unstoppable Airvent to hit shelves in early spring. On the innovation front, in collaboration with Celanese (NYSE:CE), it has created NEOLAST fiber—a more sustainable and high-performing option to last stain or spandex.

As the company repositions key products and leans into a premium, CEO Stephanie Linnartz expects a brand reinvigoration. There are green shoots, such as the North American UA Rewards Loyalty Program hitting 3 million members. Buy Under Armour stock before the turnaround gains steam.

On the date of publication, Charles Munyi did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.